For a sole trader, the annual tax return is not just a compliance form. It is a financial health check that should confirm your income, expense evidence, GST position, cash-flow exposure and growth priorities before the ATO sees the numbers.

As we approach 30 June 2026, the most efficient sole trader tax return is the one prepared progressively, not reconstructed from bank statements in October. We use a structured review process because the same data that supports lodgement also supports better pricing, cleaner cash flow, funding decisions and strategic advisory conversations.

This checklist is general in nature and based on Australian tax concepts. Your position may vary if you have employees, investment income, property, foreign clients, crypto assets, a spouse working in the business, or a business that is ready to restructure.

Why a sole trader tax return needs more than a profit figure

A sole trader reports business income and deductions through their individual tax return. There is no separate company tax return, and there is no legal separation between the individual and the business for income tax purposes.

That simplicity can be useful, but it also creates risk. A sole trader’s taxable income can include business profit, salary or wages, rental income, capital gains, interest, dividends, foreign income and other assessable amounts. The final tax outcome may also be affected by Medicare levy, HELP or study debt, PAYG instalments, personal super contributions and offsets.

The key is to reconcile the tax return back to reliable source records. In our experience, most lodgement problems are not caused by complex tax law. They are caused by incomplete income capture, weak deduction evidence, GST misclassification, private-use adjustments and poor timing around superannuation or asset purchases.

The sole trader tax return checklist

Use this checklist before lodging, or before sending your records to your accountant. It is designed for Australian sole traders, including consultants, tradies, creatives, allied health practitioners, e-commerce operators, gig workers, property-related professionals and home-based entrepreneurs.

| Checklist area | What to prepare | Why it matters |

|---|---|---|

| Identity and registrations | TFN, ABN, business name details, GST registration status and accounting software access | Confirms the correct tax profile and lodgement obligations |

| Income | Invoices, bank deposits, platform income, cash receipts, merchant settlements and foreign income | Reduces the risk of omitted income and ATO data-matching issues |

| Bank reconciliation | Business bank accounts, loan accounts, credit cards and payment gateways reconciled to 30 June | Validates that profit is based on complete transactions |

| Expenses | Supplier invoices, receipts, subscriptions, insurance, rent, utilities, software, contractor costs and materials | Supports deductions and improves audit readiness |

| GST and BAS | BAS lodged for the year, GST reports, GST coding, unpaid BAS liabilities and reconciliation to profit and loss | Ensures income tax reporting aligns with GST reporting where relevant |

| Motor vehicle | Logbook, odometer readings, kilometres, fuel, insurance, registration, repairs and finance documents | Supports business-use claims and private-use adjustments |

| Home office | Work-from-home records, dedicated workspace evidence, internet, phone, electricity and rent or occupancy considerations | Helps determine whether fixed rate or actual cost methods are appropriate |

| Assets and depreciation | Asset register, purchase dates, invoices, disposal details and finance contracts | Distinguishes repairs from capital assets and applies correct depreciation treatment |

| Stock and work in progress | Opening stock, closing stock, stocktake records, write-offs and WIP calculations | Critical for retailers, builders, manufacturers and project-based operators |

| Payroll and contractors | STP records, PAYG withholding, superannuation payments, contractor invoices and TPAR obligations if applicable | Reduces exposure to payroll, super and contractor reporting errors |

| Superannuation | Personal deductible super contributions, notice of intent documentation and employer super obligations if staff are engaged | Can affect deductions, retirement strategy and compliance |

| Private-use adjustments | Motor vehicle, phone, internet, home office, travel and mixed-use assets | Prevents overstated deductions and improves defensibility |

| Tax planning items | PAYG instalments, expected tax payable, non-commercial loss rules, PSI issues and restructuring triggers | Turns annual lodgement into a forward-looking planning exercise |

Step 1: Confirm every source of income

The ATO receives information from employers, banks, government agencies, share registries, super funds and many digital platforms. Sole traders should assume that income data is increasingly visible and cross-checkable.

Your income review should include normal invoices, cash payments, EFTPOS or merchant sales, online marketplace income, ride-share or delivery platform receipts, affiliate income, grants, rebates and foreign client payments. If you receive foreign currency, keep the conversion records and bank evidence.

For GST-registered sole traders, confirm whether income in the tax return is reported net of GST. If you are not registered for GST, the gross amount received is generally part of the income and expense records. This distinction is often overlooked when sole traders export data from accounting software without reviewing the tax settings.

Step 2: Reconcile bank accounts before reviewing deductions

A tax return built on unreconciled bank feeds is not reliable. Before analysing deductions, reconcile all business accounts to 30 June, including transaction accounts, savings accounts, credit cards, PayPal, Stripe, Square, Shopify, Afterpay-style platforms and loan accounts used for business activity.

Where personal and business transactions are mixed, the review takes longer and the risk of error increases. We generally recommend a separate business bank account for every sole trader, even where the business is small. It creates a cleaner evidence trail and gives us better data for advisory work.

A strong reconciliation should answer three questions. Did all income reach the accounts? Were all expenses categorised correctly? Are any transfers, drawings or loan movements incorrectly treated as income or deductions?

Step 3: Test deductions for evidence, nexus and private use

A deduction is not claimed simply because the business paid for something. It must have a sufficient connection to earning assessable income and be supported by records. If there is private use, the claim must be apportioned.

Common deduction categories for sole traders include accounting fees, advertising, software subscriptions, professional memberships, bank fees, business insurance, contractor costs, tools, training, protective clothing, repairs, rent for business premises, telephone, internet and travel.

Be careful with expenses that often have mixed use. Phones, vehicles, laptops, home internet and travel can be legitimate deductions, but only to the business-use extent. We prefer contemporaneous evidence, such as logbooks, diary records, usage reports and supplier invoices, over estimates made months after year-end.

Insurance is another area worth reviewing carefully. Public liability, professional indemnity and business asset insurance may be deductible where they relate to business operations. Personal insurance requires a separate analysis, because life, trauma and capital-style policies are not treated the same as income protection or business cover. If your work crosses borders, insurance requirements may also change. For example, contractors taking UAE engagements can use InsuranceHub's online insurance comparison service to compare local car, health, home or life insurance options before committing to cover.

Step 4: Review GST, BAS and income tax alignment

If you are registered for GST, your BAS history must be reconciled before lodging the income tax return. The profit and loss report will not always equal BAS totals, but differences should be explainable.

Typical reasons for differences include GST-free sales, input-taxed items, private-use adjustments, asset purchases, timing differences between cash and accrual reporting, wages, superannuation, depreciation and transactions coded to the wrong GST category.

| BAS item | Pre-lodgement check | Common issue |

|---|---|---|

| G1 sales | Compare BAS sales to accounting revenue and bank receipts | Missing cash, platform or foreign income |

| GST collected | Review GST on sales invoices and merchant transactions | GST incorrectly charged or not charged |

| GST credits | Check supplier tax invoices and business purpose | Credits claimed without valid evidence |

| PAYG withholding | Reconcile to payroll and STP records if employees exist | Payroll reports not matching BAS labels |

| BAS liabilities | Confirm all BAS are lodged and paid or recorded as liabilities | Tax return ignores unpaid ATO balances |

GST registration is generally required once your GST turnover reaches the threshold. Do not wait until the annual tax return to assess this. A growing sole trader should monitor turnover monthly, particularly in e-commerce, trades, consulting and digital services.

Step 5: Check motor vehicle and travel claims

Motor vehicle deductions remain a common ATO review area. You need to identify the correct method, support the business-use percentage and separate private travel from business travel.

For many sole traders, travel from home to a regular work location is private. Travel between job sites, client premises, suppliers or temporary work locations may be different. Tradies, allied health providers, consultants and real estate agents often have legitimate business travel, but the pattern must be documented.

Keep odometer readings at 30 June, finance documents, fuel and servicing records, insurance, registration and repair invoices. If using the logbook method, ensure the logbook is valid and reflects current business use. If using the cents-per-kilometre method, stay within the ATO rules for the relevant year and keep a reasonable basis for the kilometres claimed.

Step 6: Treat home office claims strategically

Home-based sole traders should review home office claims with care. The ATO allows different approaches, but each requires records and a clear connection to income-producing work.

A virtual assistant, designer, software developer, consultant or online retailer may have substantial home-based work. However, private household costs cannot simply be converted into business deductions. You need to identify the business-use portion, working hours and eligible cost categories.

Be particularly cautious with occupancy expenses, such as rent, mortgage interest, council rates and home insurance. These claims may have broader implications, including capital gains tax considerations for homeowners. We review these issues before the return is lodged, not after a later property sale creates an unexpected tax problem.

Step 7: Separate assets, repairs and consumables

A common mistake is treating all purchases as immediate deductions. Some items are consumables or repairs, while others are depreciating assets or capital improvements.

Examples include laptops, cameras, tools, machinery, vehicles, office furniture, medical equipment, fit-out costs and website development. The tax treatment depends on the asset, cost, use, timing and available small business concessions for the relevant income year.

Your pre-lodgement file should include purchase invoices, finance agreements, delivery dates, business-use percentages and disposal details for assets sold, traded in, scrapped or converted to private use.

Step 8: Review payroll, superannuation and contractor obligations

Sole traders who employ staff carry employer obligations, including PAYG withholding, Single Touch Payroll, superannuation guarantee and potentially workers compensation and payroll tax depending on the broader facts.

From 1 July 2025, the superannuation guarantee rate is 12%. From 1 July 2026, payday super is scheduled to significantly change the timing discipline around super payments. For sole traders with employees, this is not just a compliance issue. It is a cash-flow planning issue.

Contractor payments also need review. Some industries must lodge a Taxable Payments Annual Report, commonly called TPAR. This can apply to building and construction, cleaning, courier, road freight, IT, security, investigation or surveillance services, depending on the business activities. If contractor invoices are not properly captured, both deductions and reporting can be wrong.

Step 9: Consider PSI and non-commercial loss rules

Personal Services Income, known as PSI, can affect consultants, IT contractors, engineers, medical professionals, designers and other individuals who mainly earn income from their personal skills or efforts. PSI rules may restrict certain deductions and affect how income is treated.

Losses also require analysis. If your sole trader business made a loss, the non-commercial loss rules may prevent that loss from being immediately offset against other income unless specific tests or exceptions are met.

These rules are technical, and the answer is highly fact-dependent. We do not treat them as a final-hour tax return question. They should be reviewed before 30 June where possible, especially for professionals transitioning from employment to contracting.

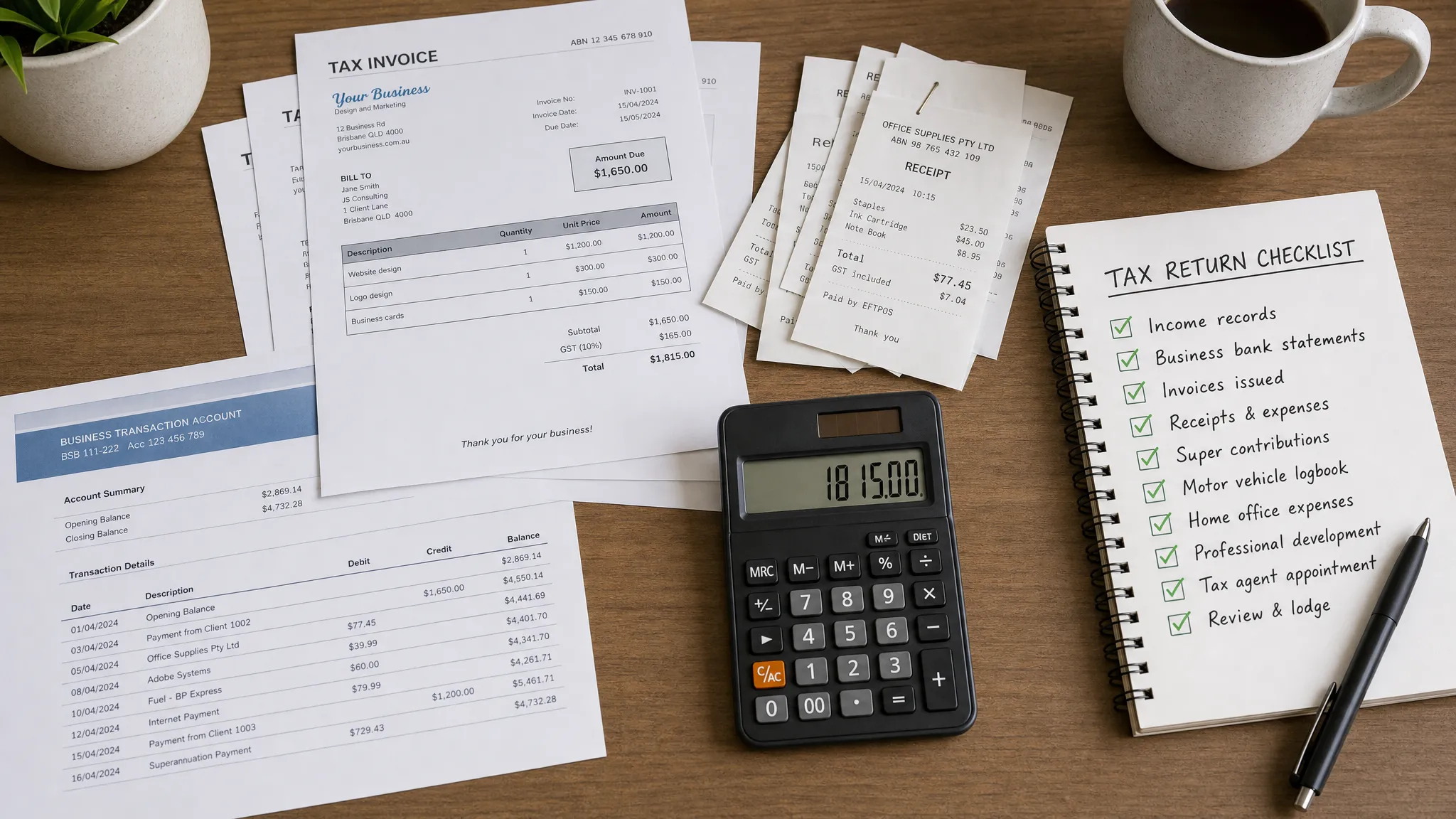

Step 10: Prepare a lodgement-ready document pack

A smoother lodgement depends on the quality of the records provided. Before sending your file to your accountant, prepare a complete pack rather than forwarding documents in fragments.

- Final profit and loss report and balance sheet, if available.

- Bank statements and reconciliations for all business accounts to 30 June.

- Copies of BAS lodged during the year and details of unpaid ATO balances.

- Invoices and receipts for major expenses, assets, insurance, rent, repairs and professional fees.

- Motor vehicle logbook, odometer readings and travel records.

- Home office working records and cost evidence.

- Payroll, STP, superannuation and contractor payment summaries if applicable.

- Stocktake, work in progress and asset register records if relevant.

- Details of personal income, investment income, rental property income, capital gains, crypto, foreign income and deductible super contributions.

The objective is not merely to lodge. The objective is to lodge with confidence, understand the tax payable and identify improvements for the next financial year.

Key dates and record-keeping reminders

If you lodge your own individual tax return, the usual deadline is 31 October after the end of the income year. If you use a registered tax agent, later lodgement dates may apply, but you generally need to be on the agent’s lodgement program in time and have your prior-year obligations up to date.

Business records generally need to be kept for five years, and some records should be retained longer, especially where they relate to assets, capital gains tax, loans or ongoing disputes. Digital records are acceptable when they are clear, accessible and reproducible.

For the 2025-26 and 2026-27 planning cycle, sole traders should also be aware that ATO interest charges are no longer deductible for income years starting on or after 1 July 2025. That makes late payment and poor tax cash-flow planning more expensive in real terms.

How automation makes sole trader lodgement smoother

We see tax compliance as a data-quality problem first and a lodgement problem second. AI-driven accounting workflows can reduce manual errors by capturing invoices, reading receipts, matching bank transactions, identifying unusual coding and producing cleaner management reports throughout the year.

Automation does not replace professional judgement. It improves the evidence base for that judgement. When bank feeds, BAS, payroll, GST coding and expense records are kept current, we can spend more time on planning questions: Should the business register for GST? Is the sole trader structure still appropriate? Are profit margins improving? Should PAYG instalments be varied? Is there a case for a company, trust or virtual CFO support as the business scales?

That is the strategic pivot. Bookkeeping is not just administration. Done properly, it becomes the foundation for tax planning, working capital control and corporate growth.

When a sole trader should seek advice before lodging

Some sole trader returns are straightforward. Others need a detailed pre-lodgement review because the tax and commercial consequences are more significant.

Seek advice early if you have rapid revenue growth, employees, unpaid super, multiple income sources, GST errors, late BAS, rental properties, crypto assets, foreign income, private-use assets, a business loss, PSI exposure, a pending ATO review, or plans to restructure.

You should also seek advice if your business is expanding across states or you need more disciplined reporting. Our team supports clients nationally, with integrated capabilities across Adelaide, Sydney and Melbourne, so the same accounting framework can be used even where operations, staff, projects and advisers are spread across multiple locations.

Frequently Asked Questions

Do sole traders lodge a separate business tax return? No. A sole trader reports business income and deductions in their individual tax return. However, the business schedule, GST position, deductions and other income sources still need careful review.

Can I claim expenses paid from my personal bank account? Potentially, yes, if the expense has a business connection and you have evidence. However, mixing personal and business transactions increases the risk of missed income, overstated deductions and slow lodgement.

Do I need to register for GST as a sole trader? GST registration is generally required once your GST turnover reaches the threshold. You should monitor turnover during the year rather than waiting until tax time.

Can a sole trader claim superannuation as a deduction? A sole trader may be able to claim a deduction for eligible personal super contributions if the required conditions are met, including giving the super fund a valid notice of intent and receiving acknowledgement.

What happens if my sole trader business made a loss? The loss may not always be immediately deductible against other income. The non-commercial loss rules can defer losses unless relevant tests or exceptions are satisfied.

How long should I keep sole trader tax records? Business records are generally kept for five years, but records connected to assets, capital gains, loans or unresolved tax matters may need to be retained longer.

Next steps for a smoother lodgement

Before lodging your next sole trader tax return, we recommend completing three actions: reconcile all business accounts to 30 June, prepare a document pack that supports income and deductions, and review whether the business structure still suits your risk, profit and growth plans.

Our team at Perfect Accounting & Tax Services combines 25 years of professional experience with AI-driven accounting workflows to help sole traders move from reactive tax filing to proactive financial management. We assist with tax returns, BAS, GST, payroll, superannuation, late lodgements, ATO matters, digital workflow implementation and strategic advisory.

If you want a cleaner lodgement and better visibility over your numbers, contact our team for a consultation. We can review your records, identify tax risks before lodgement and show you how automated accounting workflows can support more accurate, timely and strategic decision-making across Australia.