When business owners search for accounting services for business, they are usually looking for more than transaction processing. They want confidence that BAS lodgements are correct, payroll is compliant, tax positions are defensible, cash flow is visible, and decisions are supported by reliable numbers.

That is the right expectation.

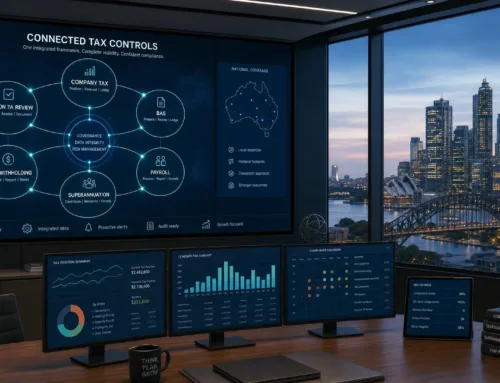

In Australia, accounting now sits at the centre of compliance, governance, automation, and strategic advisory. A modern accounting service should help directors, owners, investors, and finance teams understand what has happened, what is likely to happen next, and what actions can improve the business before tax time arrives.

We see accounting as a financial operating system. Compliance remains essential, but it should also create the data foundation for corporate growth, risk management, funding decisions, succession planning, and stronger profitability.

A proper accounting engagement should start with diagnosis

Before any meaningful work begins, an accountant should understand the commercial reality of the business. That includes structure, industry, revenue model, tax registrations, payroll profile, asset base, related entities, director loans, funding arrangements, and growth plans.

This diagnostic stage is especially important for companies, trusts, professional practices, property groups, e-commerce operators, construction businesses, hospitality groups, medical clinics, technology startups, and multi-state operators. Each has different GST, payroll, cash flow, asset, and reporting risks.

A strong onboarding process should review:

- Business structure, including sole trader, company, partnership, trust, SMSF, or group arrangements.

- ATO registrations, including ABN, TFN, GST, PAYG withholding, and fuel tax credits where relevant.

- BAS and income tax lodgement history.

- Payroll, Single Touch Payroll, superannuation, and contractor arrangements.

- Accounting software, bank feeds, invoicing systems, point-of-sale platforms, and inventory tools.

- Loans, leases, director drawings, private use, and inter-entity transactions.

- Reporting expectations for management, boards, lenders, or investors.

This is where many accounting relationships succeed or fail. If the adviser does not understand the operating model, the work becomes reactive. If they do understand it, accounting becomes a strategic control function.

Core accounting services a business should expect

The scope of accounting services will vary by business size and complexity, but most Australian businesses should expect support across several connected areas. The value is not in each task alone. The value is in how the tasks combine into one reliable financial system.

| Service area | What it should include | Strategic value |

|---|---|---|

| Bookkeeping and reconciliations | Bank feeds, invoice processing, expense coding, debtor and creditor reconciliation | Accurate data for cash flow, tax planning, and decision-making |

| BAS and GST | GST coding, BAS preparation, ATO lodgement support, review of GST adjustments | Lower risk of errors, penalties, and cash flow surprises |

| Payroll and superannuation | STP reporting, PAYG withholding, superannuation checks, payroll reconciliations | Stronger compliance and better labour cost visibility |

| Financial reporting | Profit and loss, balance sheet, cash flow reports, KPI dashboards | Better management decisions and clearer performance tracking |

| Income tax planning | Company, trust, individual, and group tax planning | More controlled tax outcomes and fewer year-end shocks |

| FBT and employee benefits | Motor vehicles, entertainment, salary packaging, reportable benefits | Reduced exposure to overlooked FBT obligations |

| Governance and compliance | ASIC records, director loans, asset registers, audit support | Better governance and stronger evidence if reviewed |

| Advisory and virtual CFO support | Forecasting, budgeting, scenario modelling, funding support | Improved profitability, working capital, and growth planning |

For directors, this breadth matters. The ATO, ASIC, lenders, investors, and boards all rely on the integrity of financial records. Weak bookkeeping can quickly become a tax issue, a cash flow issue, or a governance issue.

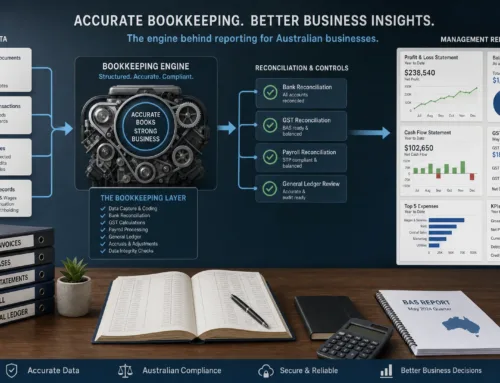

Bookkeeping should be accurate, timely, and connected

Bookkeeping is often misunderstood as basic administration. In our view, it is the foundation of financial control.

A modern bookkeeping process should not leave transactions unreconciled for months. It should capture supplier invoices promptly, reconcile bank feeds regularly, classify expenses correctly, and identify anomalies early. If the ledger is always behind, BAS becomes rushed, tax planning becomes guesswork, and management reporting loses relevance.

The ATO expects businesses to keep records that explain their transactions and tax positions. The ATO also states that business records generally need to be kept for five years, depending on the type of record and tax issue involved. Business owners can review the ATO’s guidance on record keeping for business for baseline expectations.

The practical standard should be higher than simply “keeping receipts”. We expect accounting records to be searchable, structured, secure, and linked to the underlying transaction. That is where AI-driven automation can make a significant difference.

AI-assisted workflows can help extract invoice data, flag duplicate transactions, identify unusual coding patterns, and speed up reconciliations. However, automation should not replace professional judgement. The accountant’s role is to design the system, review exceptions, interpret the numbers, and ensure the financial data supports compliant and strategic decisions.

BAS, GST, and PAYG should be managed before lodgement deadlines

BAS is not just an ATO form. It is a recurring test of the quality of your business records.

For GST-registered businesses, BAS preparation should include review of GST coding, sales reconciliation, expense classification, private use adjustments, import and export treatment, and any industry-specific GST issues. Businesses with a GST turnover of $75,000 or more generally need to register for GST, while some entities have different thresholds and requirements.

PAYG withholding also needs close attention. Payroll tax, PAYG instalments, superannuation, and STP reporting can all interact with cash flow. When these items are not reconciled regularly, directors may receive an unpleasant surprise after the quarter or at year-end.

| Compliance area | What can go wrong | What a good accountant should do |

|---|---|---|

| GST | Incorrect GST claims, missed income, poor apportionment | Review coding, reconcile sales, and check adjustments before BAS lodgement |

| PAYG withholding | Payroll figures not matching ATO reporting | Reconcile payroll reports to the ledger and STP records |

| PAYG instalments | Instalments not aligned with actual profitability | Review instalment settings and cash flow impact |

| Superannuation | Late or inaccurate contributions | Monitor super obligations and reconcile payments against payroll |

| Contractor payments | Incorrect treatment of workers or missing reporting obligations | Review contractor arrangements and reporting requirements |

For employers, Single Touch Payroll is now part of the core compliance environment. The ATO provides guidance on Single Touch Payroll reporting, but the key commercial issue is control. Payroll data should be accurate before it reaches the ATO, not corrected months later.

Payroll and superannuation require governance, not just processing

Payroll is one of the highest-risk areas in business accounting. It affects employees, directors, the ATO, super funds, workers compensation, payroll tax, and cash flow.

In the 2025-26 income year, the superannuation guarantee rate is 12%. This makes accurate payroll configuration and timely super processing even more important. For businesses with casual staff, commissions, bonuses, allowances, overtime, contractors, or multiple locations, payroll should be reviewed as a governance system rather than a routine payment run.

Accounting services for business should include checks around award interpretation inputs, superannuation settings, STP finalisation, payroll clearing accounts, leave balances, and payroll tax exposure where relevant. While employment law advice may require separate legal support, the accounting system should still provide clean, reliable payroll data.

The strategic benefit is significant. Labour is often one of the largest costs in a business. Better payroll reporting can reveal overtime pressure, margin compression, staffing inefficiency, and underperforming locations.

Management reporting should help you make decisions in real time

A year-end profit and loss statement is useful, but it is rarely enough. Directors and business owners need management reporting that shows what is happening while there is still time to respond.

The best reports are not necessarily the longest reports. They are the reports that highlight the right drivers.

For a professional services firm, that may include revenue per consultant, utilisation, debtor days, work in progress, and client profitability. For an e-commerce business, it may include gross margin, freight cost, inventory turnover, advertising spend, and return rates. For a construction business, it may include project profitability, retention amounts, subcontractor costs, and cash flow by job.

Good management reporting should connect three views:

- Profitability, including margins, overheads, and entity-level performance.

- Cash flow, including debtor collections, supplier payments, tax liabilities, and working capital.

- Balance sheet strength, including debt, assets, retained earnings, director loans, and provisions.

This is where virtual CFO services become valuable. A virtual CFO does not simply report the numbers. They help interpret the numbers, test scenarios, identify constraints, and support decisions around pricing, hiring, funding, expansion, asset purchases, and risk.

We have explored this broader control function in more detail in our article on how accounting professionals improve financial control.

Tax planning should happen before the year is over

Tax planning is most effective when there is time to act. Waiting until after 30 June limits the available options.

For Australian businesses, proactive tax planning may include reviewing profit forecasts, company tax rates, trust distributions, director remuneration, Division 7A exposure, FBT, asset purchases, bad debts, stock, losses, and timing of income and deductions. For property investors, high-net-worth individuals, and business groups, the planning may also involve CGT, land tax, financing structures, SMSF issues, and inter-entity arrangements.

A strong accountant should not treat tax planning as a once-a-year conversation. Tax planning should be integrated with cash flow forecasting. A tax saving is not useful if it creates poor working capital, weak documentation, or an ATO risk.

Directors should also be aware that ATO debt is now a more serious commercial issue. From 1 July 2025, general interest charge and shortfall interest charge incurred on or after that date are no longer deductible. This increases the cost of poor tax cash flow management and makes earlier planning more important.

For company directors, tax planning should also connect with governance. We discuss director-focused issues further in our guide to company taxes in Australia.

Advisory should turn compliance data into growth decisions

Compliance creates historical data. Advisory turns that data into action.

A strategic accounting adviser should help business owners answer questions such as:

- Which products, services, locations, or client segments generate the best margin?

- How much cash should be reserved for BAS, income tax, superannuation, payroll, and loan repayments?

- Is the current structure still appropriate for risk, growth, succession, or investment?

- Can the business afford to hire, acquire equipment, expand interstate, or take on external funding?

- Are director loans, trust distributions, or related-party transactions being managed correctly?

- What needs to change before the business seeks finance, investment, or sale?

This is the strategic pivot that separates basic compliance from high-value accounting services. The ledger becomes evidence. The reports become decision tools. The tax plan becomes part of the growth plan.

Technology should improve accuracy and visibility, not create more complexity

Many businesses have accounting software, payment apps, inventory systems, payroll platforms, and spreadsheets. The problem is not a lack of tools. The problem is often poor integration and weak data governance.

A modern accounting firm should assess the workflow end to end. That includes how invoices are raised, how expenses are approved, how documents are stored, how bank feeds are reconciled, how payroll is processed, and how reports are generated.

AI-driven automation is valuable when it removes repetitive work and highlights exceptions. It can support faster processing, cleaner records, and better real-time visibility. However, automation must be configured around Australian tax rules, the business structure, and the way management actually uses financial information.

Our approach is to use automation as a control layer, not a shortcut. The objective is not simply to reduce manual work. The objective is to improve the reliability, timeliness, and strategic usefulness of financial data.

Communication standards should be clear from the beginning

Business owners should expect a defined communication rhythm. That may be monthly reporting for a growing company, quarterly BAS and tax review meetings for an SME, or board-level reporting for a more complex group.

At minimum, an accounting relationship should clarify who is responsible for each task, when information is due, how documents should be supplied, what deadlines apply, and what decisions require director approval.

A professional accounting service should also be direct about risk. If records are incomplete, payroll is inconsistent, GST coding is unreliable, or director loans are not being managed, the accountant should raise the issue early and explain the commercial consequences.

Delayed communication creates cost. Early communication creates options.

Questions to ask before engaging an accounting firm

Selecting an accountant should not be based only on lodgement fees. The better question is whether the firm can support the complexity, risk profile, and growth ambitions of the business.

Useful questions include:

- How do you review BAS, GST, payroll, and superannuation before lodgement?

- Will we receive management reports during the year, not only annual financial statements?

- How do you use automation and AI to improve accuracy and turnaround times?

- Can you support company, trust, SMSF, property, or multi-entity structures if our affairs become more complex?

- What is your process for tax planning before 30 June?

- How do you handle ATO reviews, late lodgements, or historical clean-up work?

- Can you support us across multiple Australian locations, including Adelaide, Sydney, and Melbourne?

The right adviser should be able to explain their process clearly. If the answer is vague, the service may be reactive rather than strategic.

Red flags that your accounting service is too reactive

Many businesses outgrow their accounting support before they realise it. The signs are usually visible in delays, uncertainty, and repeated corrections.

Common red flags include late BAS preparation, unreconciled accounts, unclear GST treatment, payroll discrepancies, limited management reporting, no tax planning until year-end, no review of structure, and minimal discussion of cash flow.

Another warning sign is when the accountant only speaks to you when something is due. For growing businesses, that is not enough. Directors need current information to make decisions, not historical reports after the opportunity or risk has already passed.

How our team supports businesses across Australia

At Perfect Accounting & Tax Services, we support businesses, directors, investors, and high-net-worth individuals across Australia with integrated accounting, tax, and strategic advisory services.

Our work spans corporate and SME accounting, bookkeeping, BAS, payroll, advanced tax planning, virtual CFO advisory, audit representation, late return assistance, SMSF compliance, and industry-specific reporting. We also help businesses modernise their finance function through AI-driven automation and improved digital workflows.

With on-the-ground service capability in Adelaide, Sydney, and Melbourne, our team can support local operators, growing national businesses, and multi-city groups that need consistent financial control across locations.

We do not view compliance as the finish line. We view it as the base layer. Once the accounts are accurate, reconciled, and timely, the business can use them to improve cash flow, strengthen governance, plan tax effectively, and make better strategic decisions.

Frequently Asked Questions

What should accounting services for business include? They should include bookkeeping, BAS and GST support, payroll and superannuation checks, income tax planning, financial reporting, governance support, and strategic advisory. The exact scope depends on the structure, size, industry, and risk profile of the business.

How often should a business accountant review the accounts? For most active businesses, monthly review is ideal. At minimum, accounts should be reviewed before each BAS lodgement. Growing businesses, employers, multi-entity groups, and companies with tight cash flow often need more frequent reporting.

Is bookkeeping enough for a growing business? Bookkeeping is essential, but it is not enough on its own. A growing business also needs management reporting, tax planning, cash flow forecasting, payroll governance, and advice on structure, margins, funding, and risk.

How does automation improve business accounting? Automation can speed up invoice capture, transaction coding, reconciliations, document storage, and exception reporting. When combined with professional review, it improves accuracy, reduces delays, and gives business owners faster access to reliable financial information.

When should a business move to virtual CFO support? Virtual CFO support becomes valuable when decisions are more complex than routine compliance. This may include expansion, funding, restructuring, margin pressure, multi-location operations, board reporting, acquisition planning, or preparing a business for sale.

Next steps for stronger business accounting

If your accounting is mainly focused on deadlines, it may be time to review the system. Start by assessing whether your records are current, whether BAS and payroll are reconciled, whether you receive useful management reports, and whether tax planning is happening before year-end.

Our team can help you identify gaps, streamline your accounting workflow, and build a more strategic finance function. We can also show you how AI-driven automation can improve accuracy, reduce manual processing, and provide clearer real-time visibility across your business.

Contact Perfect Accounting & Tax Services to arrange a consultation and learn how our automated accounting workflows can support compliance, stronger financial control, and corporate growth across Adelaide, Sydney, Melbourne, and Australia-wide.